|

|||||||||

| LEAD Action News vol

11 no 1, September 2010, ISSN 1324-6011 Incorporating Lead Aware Times (ISSN 1440-4966) & Lead Advisory Service News (ISSN 1440-0561) The journal of The LEAD (Lead Education and Abatement Design) Group Inc. Editor: Anne Roberts |

|||||||||

|

About Us

|

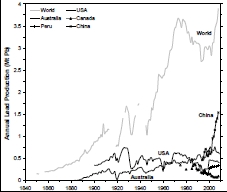

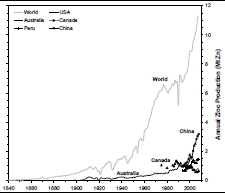

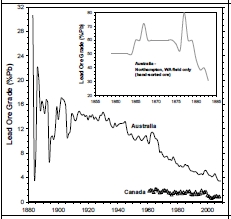

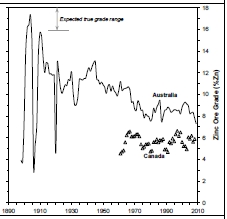

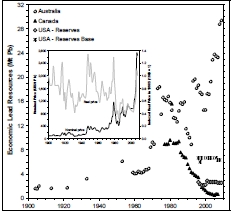

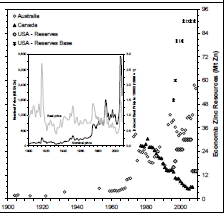

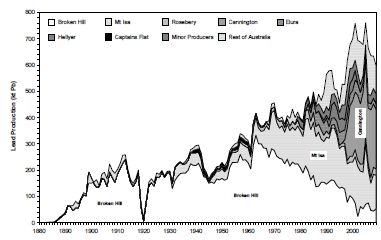

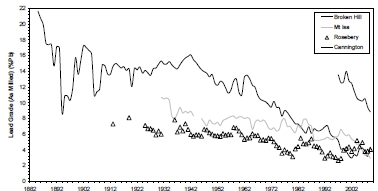

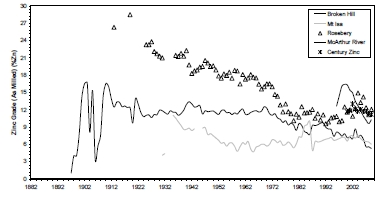

The Arrival of Peak Lead: Peak Environmental Impacts? By Dr Gavin M. Mudd, Monash University, September 2010 Lead mining is amongst one of the oldest sectors of the global mining industry, reaching back centuries in some places (even back millennia in Europe). By the mid-twentieth century, lead was ubiquitous in batteries, paints, petrol additives, chemicals, metals and alloys, and much more. By the late twentieth century, however, lead was also understood to be a recalcitrant pollutant to the environment and public health, leading to removal from paints and petrol and major recycling programs for batteries. Given that lead is a non-renewable and finite resource, there are always concerns that we may eventually run out of remaining lead deposits to mine. This, however, is only part of the issue – like ‘peak oil’, we may not run out of remaining lead deposits to mine, but they will be increasingly harder to extract and process, leading to uneconomic lead mining. As the dawn of the third millennia continues to grow, what are the key trends in primary lead production from mining? This is a brief review of some of the main mining trends which underpin the lead-zinc sector of the global mining industry. The article is based on continuing research on the sustainability of mining and its associated environmental costs, and the published peer-reviewed papers are available from the author. Lead is commonly found in hard rock sulfide deposits, usually in association with zinc (Zn) and silver (Ag), and occasionally in polymetallic deposits of lead-zinc-copper-silver-gold. These deposits are somewhat widely spread around the world, with major producers at present being China, Australia, United States, Canada, Mexico and Peru. Significant zinc is also produced by India, Kazakhstan, Sweden and Ireland. (MBendi 2010) Recent research has documented the long-term trends in lead mining in Australia (Mudd 2009a), covering the early days of hand-sorting lead ore at Northampton in Western Australia during the mid-1800s to the rise of Broken Hill, Mt Isa, Rosebery, McArthur River, Century Zinc and Cannington, amongst others. In addition, growing global data sets also examine similar trends from Canada (Mudd 2009b), with countries such as the USA, Peru and Mexico being analysed at present. The research provides important and unique insights into the evolution of an industrial sector such as lead mining. The long-term trends in global lead and zinc production are shown in Figure 1 below (top left and right graphs respectively). Curiously, by 1973 global production reached about 3.67 million tonnes (or ‘Mt’) and began a downward trend to reach just 2.7 Mt in 1993. This decline corresponds to the growing global awareness of lead’s true nature as a toxic heavy metal and declining uses. From the mid-1990s, global lead production again began to grow, led mainly by booming production from China, reaching a new high of some 3.9 Mt in 2008. In contrast, global zinc production has enjoyed a long-term steady growth. Growth was rapid following World War 2 until the mid-1970s, due mainly to rapid industrial growth in western economies, followed by slower growth until the mid-1990s when both Chinese production and consumption grew rapidly. By 2008, global zinc production had reached 11.7 Mt. The strength of zinc production over lead also shows the preferential importance miners place on zinc over lead, due to its higher price and demand. The lead production over time by mine in Australia is shown in Figure 2, clearly showing the dominance of Broken Hill, Mt Isa and more recently Cannington. The next major trends over time are ore grades – that is, how much lead and zinc is contained in each tonne of ore mined and processed. Trends in ore grades for Australia and Canada are shown in Figure 1 (middle left and right graphs). For Australia, the ore grades are dominated by large fields such as Broken Hill, Mt Isa and Rosebery, and more recently by Century Zinc, Cannington, Golden Grove and McArthur River. The ore grades of Australia’s mines over time are shown in Figure 3. The obvious trend is a long-term decline in lead grade, plus a lesser decline in zinc grade. In Canada, lead production has historically been dominated by a small number of major fields and mines, such as the Kimberley-Sullivan field of British Columbia, Brunswick and Heathe-Newcastle in New Brunswick, Faro and Keno-Elsa in Yukon, Polaris, Baffin Island and Pine Point in the Northwest Territories, and a range of minor producers such as copper-zinc mines and districts (especially in Quebec and Manitoba). Ore grades are crucial to monitor, since they are fundamental to understanding the economic costs of lead production as well as environmental costs and impacts. For example, to produce one tonne of lead from 10% Pb ore takes 10 tonnes of ore, while 1% Pb ore requires 100 tonnes of ore. As grades decline, energy costs increase and so do greenhouse gas emissions and water requirements, plus more mine waste is produced such as tailings (rock remaining after lead-zinc extraction, normally some 80-90% of the ore), plus any waste rock produced from open cut or underground mines. Waste rock has no metals of economic value, but is often problematic from an environmental perspective due to its sulfide content – which gives the waste rock a strong propensity to leach pollution via ‘acid and metalliferous drainage’ (AMD). That is, the sulfide minerals in the mine wastes can undergo chemical reactions to convert to sulfuric acid, leaching extremely high concentrations of salts and heavy metals into the environment. Thus, as ore grades continue to inevitably decline, the environmental burden increases – both in energy, greenhouse and water terms given the greater amount of ore required, but especially in terms of the legacy of mine waste to manage and rehabilitate following mining (Mudd 2010). The final critical trend is remaining economic lead-zinc resources, also shown in Figure 1 (bottom left and right graphs). The data includes Australia, Canada and the USA, each providing sharply contrasting trends. Over time, Australia has been quite successful in mineral exploration, leading to a strong growth in economic lead-zinc resources over time, especially for zinc. In the 1990s, major new deposits were discovered and developed at Century Zinc and Cannington in Queensland, with significant growth in resources at existing fields also. In contrast, Canada shows a long-term and seemingly inevitable decline, especially for lead. There has been no major new discovery in Canada for some time, with most being somewhat small to moderate. If one examines all mineral resources reported by lead mining companies in Canada, a much higher remaining resource can be estimated, although the declining trend over time would still effectively be similar. The USA appears to be somewhere in the middle, although the US Geological Survey estimates are somewhat coarse and considered order of magnitude only. For major mines and fields across the world, some have remained in production for more than a century – even at global scales of annual production (eg. Broken Hill, Kimberley-Sullivan). In contrast, numerous projects have closed after some decades, due to exhaustion of ore resources (eg. Polaris, Heathe-Newcastle). If the trends in lead-zinc production growth continue, it is clear that even Australia’s lead-zinc industry is not immune – major mines such as Century and Cannington have about a decade or two remaining, respectively. Historically speaking, this situation is not unusual nor unprecedented – the Broken Hill field for most of its early years only had a decade or two of resources remaining, a pattern it maintains even by 2010. The longer that the trend of growing production (and demand) continues, the harder and harder it gets to maintain growing production through new discoveries, technology and economics. All of these trends point to the emerging application of ‘peak curves’ to minerals – following the increasing acceptance of the peak oil problem. That is, as new deposits become harder to find and mine or process, as ore grades decline, and as demand continues to grow, this will inevitably lead to a maximum production rate from mines before a painful and perhaps permanent decline. Of course, this does not necessarily mean that the world will run out of lead – indeed, given the massive stock of already mined lead in widespread use around the world, there are good options for the future such as more aggressive recycling, more efficient use, as well as substitution where possible and realistic. A final point to consider is the environmental impacts of lead-zinc mining specifically: although uses can often result in widespread public health or environmental problems (eg. paints, petrol additives), the actual mining and primary processing stages are also significant sources of impacts. At many historic and current lead mine and smelter sites in Australia there are ongoing sagas of soil, water and/or air contamination. For example, recent research at the Mt Isa complex has shown that the lead contamination in soils which is linked to elevated blood lead levels in children is unequivocally related to historic and current lead emissions from the lead mine and smelter (Taylor et al 2010). It has taken extensive work over more than three decades at the Port Pirie lead smelter site to address lead emissions and blood lead levels in children, but the problem is still not completely solved. Perhaps the most remarkable example of all is the Magellan lead mine in central Western Australia – it was opened in 2005 but by early 2007 it was proved that its concentrate, trucked to Esperance for overseas shipping, had caused massive environmental contamination. As grades decline, this will require even greater volumes of ore to be mined and processed, placing substantive upward pressure on the cumulative environmental impacts of lead production. Although global lead production will soon ‘peak’ sometime by the middle of this century (optimistically speaking), it is clear that the cumulative environmental impacts of lead mining will continue to grow well beyond this unless there is pro-active intervention by industry, government and the community. In this regard, it is important to understand these key trends in lead production – declining ore grades, increasing mine wastes and environmental footprints – since they will become increasingly important to recognise as the world’s population continues to grow and consumption rises. Let us hope that we can address the potential environmental and public health impacts more successfully than in the past.

Figure

1: Lead and zinc production over time (top); Ore grades over time

(middle); Economic resources over time (bottom), with nominal and real

(US$1998)

Figure 2: Lead production by mine for Australia over time

Figure 3: Lead-zinc ore grades for Australia over time REFERENCES MBendi Information Services (Pty) Ltd (2010) Pb & Zn Commodity Properties and Uses; Facilities linked to World Zinc and Lead Mining (174); [including Facilities, Projects, Mining and Production of Lead and Zinc, Companies and Organisations linked to World Zinc and Lead Mining, as well as Continents and Countries with Zinc and Lead Mining Profiles, etc] www.mbendi.com/indy/ming/ldzc/p0005.htm#5 Accessed 19 September 2010. Mudd, G M (2009a), The Sustainability of Mining in Australia: Key Production Trends and Their Environmental Implications for the Future. Research Report No RR5, Department of Civil Engineering, Monash University and Mineral Policy Institute, Revised – April 2009. Mudd, G M (2009b), Historical Trends in Base Metal Mining: Backcasting to Understand the Sustainability of Mining. Proc. “48th Annual Conference of Metallurgists”, Canadian Metallurgical Society, Sudbury, Canada, August 2009. Mudd, G M (2010), The Environmental Sustainability of Mining in Australia: Key Mega-Trends and Looming Constraints. Resources Policy, 35 (2), pp 98-115. AVAILABLE FOR PURCHASE FROM http://dx.doi.org/10.1016/j.resourpol.2009.12.001 Taylor, M P; Mackay, A K; Hudson-Edwards, K A; and Holz, E (2010), Soil Cd, Cu, Pb and Zn contaminants around Mount Isa city, Queensland, Australia: Potential sources and risks to human health. Applied Geochemistry, 25, pages 841-855. AVAILABLE FOR PURCHASE FROM http://dx.doi.org/10.1016/j.apgeochem.2010.03.003 |

||||||||

|

About

Us |

bell

system lead poisoning |

Contact Us

| Council

LEAD Project | egroups | Library

- Fact Sheets | Home

Page | Media Releases Newsletters | Q & A | Referral lists | Reports | Site Map | Slide Shows - Films | Subscription | Useful Links | Search this Site |

|||||||||

|

Last

Updated 23 January 2012

|

|||||||||